| MARKET CONDITION PROFILE: Pitney Bowes, Inc. (NYSE: PBI) |

There's no denying that more often than not, the stock market can behave exactly like a 14-year-old: surprising and delighting at times but frustrating and inexplicable at others. You'll see a great stock with a solid business operation and a history of attractive dividend payments. Then, for whatever reason, the market decides it doesn't like the stock. Until it falls in love with it again.

Such is the case with postage meter titan Pitney Bowes (NYSE: PBI). Covering this stock is becoming an annual exercise of mine. I've never stopped noticing the company and the stock. But now the market is starting to catch on, too.

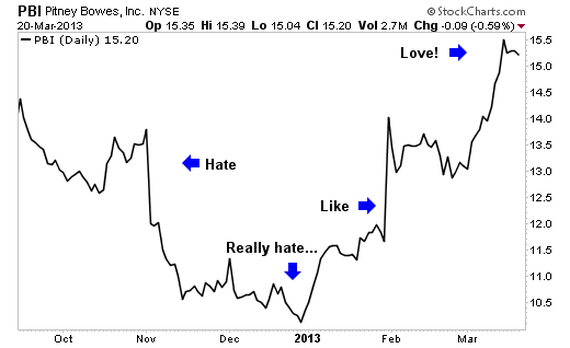

If you were a believer of the upside potential for this stock at $10.50 a share, then you've made nearly 50% on your investment, not counting the nearly 10% dividend yield you're collecting for being smart.

But is it too late to jump in? No. The company continues its metamorphosis from an old-line, manufacturing caterpillar to a beautiful, high-tech butterfly.

The writing on the wall

More than a decade ago, Xerox (NYSE: XRX) and IBM (NYSE: IBM) made a wise and conscious decision to transform themselves from hardware manufacturing companies to software and service enterprises. Take a look at what happened to IBM as a result of the change.

If you were a believer of the upside potential for this stock at $10.50 a share, then you've made nearly 50% on your investment, not counting the nearly 10% dividend yield you're collecting for being smart.

But is it too late to jump in? No. The company continues its metamorphosis from an old-line, manufacturing caterpillar to a beautiful, high-tech butterfly.

The writing on the wall

More than a decade ago, Xerox (NYSE: XRX) and IBM (NYSE: IBM) made a wise and conscious decision to transform themselves from hardware manufacturing companies to software and service enterprises. Take a look at what happened to IBM as a result of the change.

In 1993, IBM was flat on the mat. It appointed Lou Gerstner as CEO to take over and begin the company's transition.

Two decades later, after selling its PC business to Lenovo in 2004, IBM's information technology services represent more than 50% of revenue. Smart investors who believed in the company's transformation have earned an annual average of 65% during the past 20 years before dividends. Now Pitney Bowes is following the same model. In December 2012, Pitney's board hired Marc B. Lautenbach as president and CEO. Ironically, Lautenbach has spent the past 30 years of his career at IBM.

Out with the old and in with the new

Pitney's "new" business is hardly an old-line business. Primarily, it's software driven. The cornerstone is an e-commerce/cloud platform the company has been ramping up quietly but steadily. Pitney also provides geolocation software that powers Facebook's "check in" feature.

According to my source inside the company, there are no current or articulated plans to spin off or sell the postage hardware business. However, doing so would generate an enormous pile of cash the company could use to expand the software/service business or even return to the shareholders in the form of dividends or stock buyback. Pitney's previous management also implemented a restructuring program in 2009 that is starting to bear fruit. Among the main changes, the company sold off its international mailing business to a private equity firm. I think that was a test run for the future.

The results of the turnaround

The company reported 2012 revenue of $4.9 billion, a decrease from $5.3 billion in 2011. This was mainly due to the continuing decline of physical mail as a communication medium. Its "new" business of software and services contributed 53.2% while hardware postage meters and related products from the "old" business contributed 46.5% to the cause.

And although these two divisions contribute about the same toward revenue, the real story is in the company's profit margins. The old business earned a gross profit margin of just about 2% in 2012, while the new business turned in gross margins of nearly 20%.

Take into account that Pitney has been able to retire more than $500 million in debt during the past two years. It has also bought back 4.7 million shares of its stock, a transaction worth up to $50 million. Its dividend has also been rising each year for the last 24 years. With all of this in mind, Pitney Bowes shares offer an excellent opportunity in the near and long term.

Two decades later, after selling its PC business to Lenovo in 2004, IBM's information technology services represent more than 50% of revenue. Smart investors who believed in the company's transformation have earned an annual average of 65% during the past 20 years before dividends. Now Pitney Bowes is following the same model. In December 2012, Pitney's board hired Marc B. Lautenbach as president and CEO. Ironically, Lautenbach has spent the past 30 years of his career at IBM.

Out with the old and in with the new

Pitney's "new" business is hardly an old-line business. Primarily, it's software driven. The cornerstone is an e-commerce/cloud platform the company has been ramping up quietly but steadily. Pitney also provides geolocation software that powers Facebook's "check in" feature.

According to my source inside the company, there are no current or articulated plans to spin off or sell the postage hardware business. However, doing so would generate an enormous pile of cash the company could use to expand the software/service business or even return to the shareholders in the form of dividends or stock buyback. Pitney's previous management also implemented a restructuring program in 2009 that is starting to bear fruit. Among the main changes, the company sold off its international mailing business to a private equity firm. I think that was a test run for the future.

The results of the turnaround

The company reported 2012 revenue of $4.9 billion, a decrease from $5.3 billion in 2011. This was mainly due to the continuing decline of physical mail as a communication medium. Its "new" business of software and services contributed 53.2% while hardware postage meters and related products from the "old" business contributed 46.5% to the cause.

And although these two divisions contribute about the same toward revenue, the real story is in the company's profit margins. The old business earned a gross profit margin of just about 2% in 2012, while the new business turned in gross margins of nearly 20%.

Take into account that Pitney has been able to retire more than $500 million in debt during the past two years. It has also bought back 4.7 million shares of its stock, a transaction worth up to $50 million. Its dividend has also been rising each year for the last 24 years. With all of this in mind, Pitney Bowes shares offer an excellent opportunity in the near and long term.

Risks to consider: Many factors could derail the company's future. Among them would be a softening of the country's evident economic recovery, failure to execute the turnaround plan, or just the sheer unwillingness of those within the organization to change. Luckily, the stock's low valuation, strong free cash flow and fat dividend offer some downside protection.

Action to take --> Having said that, with the IBM background the new CEO has, the odds look good for Pitney Bowes. The shares have had an amazing 44% climb in the first quarter of this year, but there's still room to move. The stock currently trades at around $15.40, yields close to 10% and has a forward price-to-earnings (P/E) ratio of 7.9, which is less than half that of the S&P 500.

Based on the turnaround strategy in place, shares could climb to $20 during the next 12 months, resulting in a forward P/E expansion to 9. That would be a nearly 30% upside from current levels. Throw in the dividend yield and the potential total return is closer to 40%. However, if the transition is successful, then the potential returns could be much richer in the longer term.

Action to take --> Having said that, with the IBM background the new CEO has, the odds look good for Pitney Bowes. The shares have had an amazing 44% climb in the first quarter of this year, but there's still room to move. The stock currently trades at around $15.40, yields close to 10% and has a forward price-to-earnings (P/E) ratio of 7.9, which is less than half that of the S&P 500.

Based on the turnaround strategy in place, shares could climb to $20 during the next 12 months, resulting in a forward P/E expansion to 9. That would be a nearly 30% upside from current levels. Throw in the dividend yield and the potential total return is closer to 40%. However, if the transition is successful, then the potential returns could be much richer in the longer term.

RSS Feed

RSS Feed