| MARKET CONDITIONS PROFILED: Universal Corp. (NYSE: UVV) British American Tobacco (NYSE: BTI) |

A recent article by Joseph Hogue on the "hated" company Philip Morris (NYSE: PM) reminded me of the incident at the ballpark. I learned that despite this company's leading position in a pariah of an industry, it is held by nearly 1,400 institutional funds and has consistently outperformed the market. This revelation sparked my interest in looking behind Philip Morris for other top-performing companies in the tobacco industry.

Over the years, I have learned that for every successful and popular stock, there are usually several under-the-radar companies that are also thriving on the success of the well-known name. These companies can be competitors, partners, or critical links in the supply chain.

My digging revealed a quality dividend-paying stock that's part and parcel of Philip Morris's supply chain. Although it is nowhere as well known as Philip Morris, this company plays a critical behind-the-scenes role in Philip Morris' success.

The company is Universal Corp. (NYSE: UVV), a Richmond, Va.-based tobacco merchant and processor with operations in more than 30 countries. Working directly with manufacturers of tobacco-based products, Universal specializes in the financing, selection, processing and storage of leaf tobacco.

Founded in 1918, the company boasts a market cap of nearly $1.5 billion and a forward price-to-earnings (P/E) ratio of just over 12. Universal just posted improved annual results with net income rising 44% to nearly $133 million from last year and operating income up 4% to close to $233 million on revenue of $2.5 billion. The company currently pays a quarterly dividend of 50 cents, which equates to a yield of about 3.5%. The company has increased its dividend for 42 years in a row, making for an enticing long-term investment.

Universal's customers include Philip Morris, British American Tobacco (NYSE: BTI) and Imperial Tobacco (OTC: ITYBY). It has been able to maintain its profits by sourcing tobacco to meet demand. In other words, most of its inventory is already committed to sale. This intelligent strategy helps insulate Universal from the pressure of commodity price risk.

Over the years, I have learned that for every successful and popular stock, there are usually several under-the-radar companies that are also thriving on the success of the well-known name. These companies can be competitors, partners, or critical links in the supply chain.

My digging revealed a quality dividend-paying stock that's part and parcel of Philip Morris's supply chain. Although it is nowhere as well known as Philip Morris, this company plays a critical behind-the-scenes role in Philip Morris' success.

The company is Universal Corp. (NYSE: UVV), a Richmond, Va.-based tobacco merchant and processor with operations in more than 30 countries. Working directly with manufacturers of tobacco-based products, Universal specializes in the financing, selection, processing and storage of leaf tobacco.

Founded in 1918, the company boasts a market cap of nearly $1.5 billion and a forward price-to-earnings (P/E) ratio of just over 12. Universal just posted improved annual results with net income rising 44% to nearly $133 million from last year and operating income up 4% to close to $233 million on revenue of $2.5 billion. The company currently pays a quarterly dividend of 50 cents, which equates to a yield of about 3.5%. The company has increased its dividend for 42 years in a row, making for an enticing long-term investment.

Universal's customers include Philip Morris, British American Tobacco (NYSE: BTI) and Imperial Tobacco (OTC: ITYBY). It has been able to maintain its profits by sourcing tobacco to meet demand. In other words, most of its inventory is already committed to sale. This intelligent strategy helps insulate Universal from the pressure of commodity price risk.

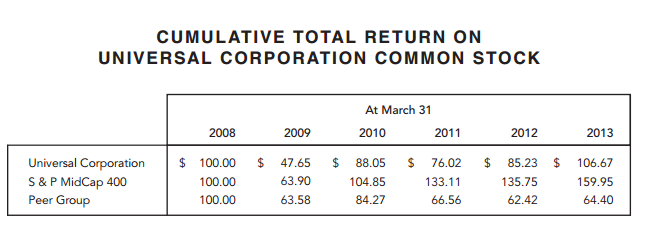

As you can see, Universal has outperformed its peer group over the past five years. Universal isn't a fast-rising growth stock, but it is a solid, dividend producing company that deserves a place in every long term dividend growth portfolio.

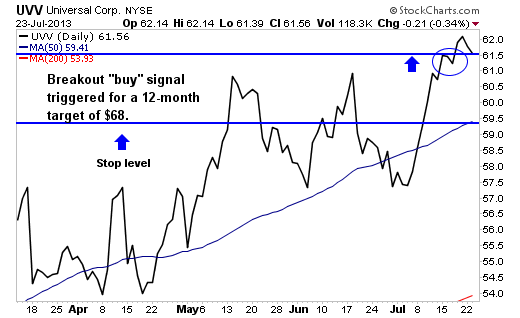

Technically, shares have been trending up from a double bottom formed in April. Price has set up to be an ideal buy as a breakout entry above $61.50. My 12-month target price is $68 with an initial stop level at the 50-day simple moving average of $59.50.

Risks to Consider: Despite its strong performance, Universal remains in a pariah industry. As seen in the United States, consumer tastes can rapidly change, and possible governmental regulations and anti-smoking measures could damage profits. In addition, it's important to note that leaf tobacco usage has been slowly declining. Although the company's inventory methods work to reduce commodity price risk, this risk still remains as a possible headwind.

Action to Take --> I like Universal right now as a long-term investment. Always remember to use stops and that diversification is the key to consistent stock market profits.

Risks to Consider: Despite its strong performance, Universal remains in a pariah industry. As seen in the United States, consumer tastes can rapidly change, and possible governmental regulations and anti-smoking measures could damage profits. In addition, it's important to note that leaf tobacco usage has been slowly declining. Although the company's inventory methods work to reduce commodity price risk, this risk still remains as a possible headwind.

Action to Take --> I like Universal right now as a long-term investment. Always remember to use stops and that diversification is the key to consistent stock market profits.

RSS Feed

RSS Feed