| MARKET CONDITIONS People have asked me on multiple occasions, "What should I be in now? How long should I hold the position?", etc. My answer to how long to hold a position is simple...when it stops being profitable. That's why trailing stops exist. As far as what to be in now, I frequently update this section, Commodities Corner and Retire Rich with recommendations that we ALL should be invested in, especially when there are dividends in our future. However, the recommendations here didn't seem to be enough for some of you out there. OK, here it is...a short addendum of what to be in right NOW. |

According to 13F filings, Billionaire T. Boone Pickens has taken a sizable position with the following companies: Apache (NYSE: APA), Tesoro (NYSE: TSO), Marathon Petroleum (NYSE: MPC), Gulfport Energy (Nasdaq: GPOR) and Phillips 66 (NYSE: PSX).

As you might expect, these stocks have all done well this year. Gulfport has seen the biggest gains, up 28%. The only laggard of the bunch is Apache, up "only" 8%. So, considering the big gains we've already seen in this sector, are any of these picks still a good investment at today's prices?

While I strongly believe all five companies should remain on investors' short list of stocks to watch, I think Phillips 66 offers the best value at today's prices. Phillips' strength lies in the diversification of its assets. Although it is known primarily as a refiner, the company also owns interests in pipelines and chemical assets that help boost earnings and provide stability, and help to differentiate the company from its peers.

As part of a joint venture with Spectra Energy (NYSE: SE), Phillips owns a 50% interest in DCP Midstream Partners (NYSE: DPM). DPM owns or operates 62 natural gas processing facilities and 12 NGL fractionation plants. And it services these facilities through its massive, 62,000 mile natural gas pipeline system.

If you read my postings on LNG and MLPs, you are probably already familiar with my fondness for "irreplaceable" assets like pipelines. These assets are very difficult to replicate, which discourages competition and helps maximize profits. Brookfield Infrastructure (NYSE: BIP) is up more than 48% since my earlier recommendation. In addition to its position in DPM, Phillips holds other midstream assets, including a 25% interest in the REX pipeline and investments in fractionation plants.

Although Phillips has been publicly traded only since May 2012, it has already increased its dividend twice. It currently pays a rate of 31 cents a share, which comes out to a yield of 1.78% at today's prices. The company's core refinery business also continues to churn out profits. Phillips operates a total of 15 refineries, 11 of which are in the U.S. It also operates one refinery in each of Malaysia, Germany, the U.K. and Ireland. (In fact, the Whitegate plant in Ireland is the only refining facility of its kind in that country.)

The amount of free cash flow the company generates has grown enormously over the past three years. During the past 12 months, PSX reported almost $5 billion in free cash flow, a fivefold increase over the $946 million reported in 2010. Free cash flow is an important metric to consider because it indicates that a company has cash to expand, develop new products, buy back stock and pay dividends. Rising free cash flow is a good indicator of a healthy, thriving company.

T. Boone Pickens is not alone in his fondness for PSX. Warren Buffett's Berkshire Hathaway (NYSE: BRK-B) owns over 27 million shares of the company -- an investment of more than $1.9 billion. As they say -- great minds think alike.

Risks to Consider: In December, PSX announced it would form a master limited partnership (MLP) sometime in the second half of this year. Transportation and terminal assets typically do well as MLPs, and some of these assets are likely to be the foundation for Phillips' new entity. However, if PSX decides to consolidate all or some of its pipeline assets into an MLP, it could damage diversification and reduce one of the company's key advantages.

Action to Take --> PSX is currently trading at a forward price-to-earnings ratio of 7.4 and a price-to-book ratio of 1.8, both of which are slightly lower than the industry average. The stock rates a buy below $60 per share. Much like Phillips 66, Brookfield Infrastructure deals in long-lived, irreplaceable assets and we thinks Brookfield's headed for big things in the coming years.

Supply and demand is what drives the global economic engine. Imagine owning a company whose products and services have nearly guaranteed steady demand and government-regulated supply. Add in the beauty of government-supported monopoly-like power and steady dividend yields and you've attained investor nirvana.

Although these companies may be considered boring and overlooked by investors seeking rapid capital appreciation, they remain an ace in the hole for long-term stock investors. If you haven't guessed, I'm talking about utility stocks. Despite a recent pullback, these consistent and proven dividend machines are ideal "buy" candidates for any long-term portfolio. With this in mind, here are my two favorite utility stocks:

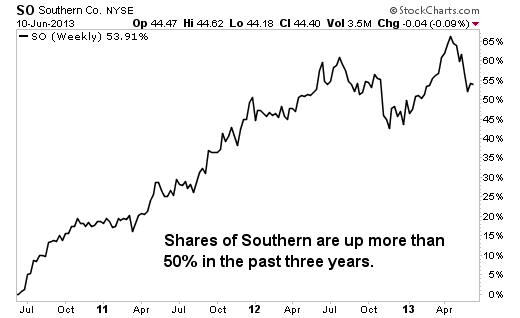

Southern Co. (NYSE: SO)

A leading U.S. provider of electricity, this large-cap public electric utility has a market capitalization of more than $38 billion and boasts a price-to-earnings (P/E) ratio of nearly 19. Southern has subsidiaries in four states, including Mississippi Power, Georgia Power, Gulf Power and Alabama Power.

The company's beta is -0.10, meaning it's nearly as volatile as the overall market, and its stock currently yields more than 4% annually. Profitability has increased from close to $2 billion in 2010 to more than $2.1 billion in 2012, indicating an enhancement of more than 4%.

As you might expect, these stocks have all done well this year. Gulfport has seen the biggest gains, up 28%. The only laggard of the bunch is Apache, up "only" 8%. So, considering the big gains we've already seen in this sector, are any of these picks still a good investment at today's prices?

While I strongly believe all five companies should remain on investors' short list of stocks to watch, I think Phillips 66 offers the best value at today's prices. Phillips' strength lies in the diversification of its assets. Although it is known primarily as a refiner, the company also owns interests in pipelines and chemical assets that help boost earnings and provide stability, and help to differentiate the company from its peers.

As part of a joint venture with Spectra Energy (NYSE: SE), Phillips owns a 50% interest in DCP Midstream Partners (NYSE: DPM). DPM owns or operates 62 natural gas processing facilities and 12 NGL fractionation plants. And it services these facilities through its massive, 62,000 mile natural gas pipeline system.

If you read my postings on LNG and MLPs, you are probably already familiar with my fondness for "irreplaceable" assets like pipelines. These assets are very difficult to replicate, which discourages competition and helps maximize profits. Brookfield Infrastructure (NYSE: BIP) is up more than 48% since my earlier recommendation. In addition to its position in DPM, Phillips holds other midstream assets, including a 25% interest in the REX pipeline and investments in fractionation plants.

Although Phillips has been publicly traded only since May 2012, it has already increased its dividend twice. It currently pays a rate of 31 cents a share, which comes out to a yield of 1.78% at today's prices. The company's core refinery business also continues to churn out profits. Phillips operates a total of 15 refineries, 11 of which are in the U.S. It also operates one refinery in each of Malaysia, Germany, the U.K. and Ireland. (In fact, the Whitegate plant in Ireland is the only refining facility of its kind in that country.)

The amount of free cash flow the company generates has grown enormously over the past three years. During the past 12 months, PSX reported almost $5 billion in free cash flow, a fivefold increase over the $946 million reported in 2010. Free cash flow is an important metric to consider because it indicates that a company has cash to expand, develop new products, buy back stock and pay dividends. Rising free cash flow is a good indicator of a healthy, thriving company.

T. Boone Pickens is not alone in his fondness for PSX. Warren Buffett's Berkshire Hathaway (NYSE: BRK-B) owns over 27 million shares of the company -- an investment of more than $1.9 billion. As they say -- great minds think alike.

Risks to Consider: In December, PSX announced it would form a master limited partnership (MLP) sometime in the second half of this year. Transportation and terminal assets typically do well as MLPs, and some of these assets are likely to be the foundation for Phillips' new entity. However, if PSX decides to consolidate all or some of its pipeline assets into an MLP, it could damage diversification and reduce one of the company's key advantages.

Action to Take --> PSX is currently trading at a forward price-to-earnings ratio of 7.4 and a price-to-book ratio of 1.8, both of which are slightly lower than the industry average. The stock rates a buy below $60 per share. Much like Phillips 66, Brookfield Infrastructure deals in long-lived, irreplaceable assets and we thinks Brookfield's headed for big things in the coming years.

Supply and demand is what drives the global economic engine. Imagine owning a company whose products and services have nearly guaranteed steady demand and government-regulated supply. Add in the beauty of government-supported monopoly-like power and steady dividend yields and you've attained investor nirvana.

Although these companies may be considered boring and overlooked by investors seeking rapid capital appreciation, they remain an ace in the hole for long-term stock investors. If you haven't guessed, I'm talking about utility stocks. Despite a recent pullback, these consistent and proven dividend machines are ideal "buy" candidates for any long-term portfolio. With this in mind, here are my two favorite utility stocks:

Southern Co. (NYSE: SO)

A leading U.S. provider of electricity, this large-cap public electric utility has a market capitalization of more than $38 billion and boasts a price-to-earnings (P/E) ratio of nearly 19. Southern has subsidiaries in four states, including Mississippi Power, Georgia Power, Gulf Power and Alabama Power.

The company's beta is -0.10, meaning it's nearly as volatile as the overall market, and its stock currently yields more than 4% annually. Profitability has increased from close to $2 billion in 2010 to more than $2.1 billion in 2012, indicating an enhancement of more than 4%.

Southern has plans to invest $14 billion over the next several years to increase transmission and power-generating capacity. In addition, the company is targeting earnings growth of 5% to 7% for each of the next five years.

What I like best about this utility is the fact that Southern investors are enjoying much faster dividend growth than the majority of other utilities. The company has grown at an astounding rate of 40% over the past 10 years, yet the payout ratio remains at less than 30% of cash flow, which means future dividend growth is probable. Presently throwing off a forward annual yield of 4.6%, this utility is an excellent prospect for long-term investors.

Duke Energy (NYSE: DUK)

The largest electric company in the United States, Duke provides electricity to more than 7 million homes in the Carolinas, the Midwest and Florida. The company also provides natural gas distribution services in Ohio and Kentucky, as well as diverse power generation and renewable-energy assets in Latin America and North America.

Over the past three years, Duke's net profits have increased from roughly $1.3 billion in 2010 to more than $2.1 billion this year. The company currently boasts a beta of 0.08 and an annual yield of 4.5%.

What I like best about this utility is the fact that Southern investors are enjoying much faster dividend growth than the majority of other utilities. The company has grown at an astounding rate of 40% over the past 10 years, yet the payout ratio remains at less than 30% of cash flow, which means future dividend growth is probable. Presently throwing off a forward annual yield of 4.6%, this utility is an excellent prospect for long-term investors.

Duke Energy (NYSE: DUK)

The largest electric company in the United States, Duke provides electricity to more than 7 million homes in the Carolinas, the Midwest and Florida. The company also provides natural gas distribution services in Ohio and Kentucky, as well as diverse power generation and renewable-energy assets in Latin America and North America.

Over the past three years, Duke's net profits have increased from roughly $1.3 billion in 2010 to more than $2.1 billion this year. The company currently boasts a beta of 0.08 and an annual yield of 4.5%.

Risks to Consider: Utilities are widely considered to be among the safest, best-yielding stock investments available. However, a recent study has made it clear that utility stocks may actually be more volatile, as a whole, than the overall stock market.

While this in no way negates the power of utility stocks as dividend-producing machines, it shows that utilities may share similar risks as the rest of the stock market. As always, choose your investments carefully and be sure to diversify.

Action to Take --> On the daily technical chart, Duke and Southern appear nearly identical. They have followed a lockstep pattern of falling from the highs, breaking below the crucial technical support of the 200-day simple moving average, then bouncing back above resistance, setting up an ideal buying level.

My 12-month targets are $75 for Duke Energy and $50 for Southern.

You would think a master limited partnership (MLP) that has outperformed its industry peers by 88% and the Nasdaq by 34% in the past five years -- while yielding an average of 8.8% -- would be well-known to investors but this MLP flies under the radar. No Wall Street analysts follow this company, and institutions hold only 11% of its shares. However, if you're looking for a profitable high yielder poised for growth from rising energy prices, this is a name you should know.

The stock I'm talking about is Dorchester Minerals (Nasdaq: DMLP), an energy MLP formed in 2003 through a merger of three smaller companies. Dorchester generates revenue from royalties it collects from the oil and gas wells on its properties, which total 3 million acres spread across 25 states. Dorchester has exposure to many of North America's most prolific gas fields, including the Fayetteville Shale, the Bakken formation, the Appalachian Basin, the Barnett Shale, the Permian Basin and the Granite Wash.

Perhaps best of all, only about 30% of Dorchester's holdings are developed. That adds to the potential for a rising income stream as new wells are drilled. Unlike conventional oil and gas drillers, Dorchester has no exposure to the costs and risks of exploration, development and production. Instead, the company collects a royalty based on the sales volume of each well after the driller recoups 150% of well expenses because royalty payments are directly affected by the selling price of natural gas.

Dorchester generates more cash flow when natural gas prices are rising. Dorchester also differs from many of its MLP peers in that its general partner's fee is fixed at 4%. There are no distribution rights or incentives that increase the general partner's percentage on higher profits. Dorchester unit holders can count on consistently collecting 96% of the MLP's cash flow.

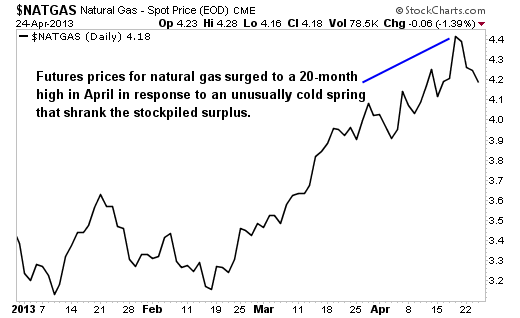

The improving outlook for natural gas demand and prices means this may be an especially good time to own Dorchester. Futures prices for natural gas surged to a 20-month high in April in response to an unusually cold spring that drained stockpiles. This prompted Goldman Sachs to raise its outlook for 2013 natural gas prices by 17%.

While this in no way negates the power of utility stocks as dividend-producing machines, it shows that utilities may share similar risks as the rest of the stock market. As always, choose your investments carefully and be sure to diversify.

Action to Take --> On the daily technical chart, Duke and Southern appear nearly identical. They have followed a lockstep pattern of falling from the highs, breaking below the crucial technical support of the 200-day simple moving average, then bouncing back above resistance, setting up an ideal buying level.

My 12-month targets are $75 for Duke Energy and $50 for Southern.

You would think a master limited partnership (MLP) that has outperformed its industry peers by 88% and the Nasdaq by 34% in the past five years -- while yielding an average of 8.8% -- would be well-known to investors but this MLP flies under the radar. No Wall Street analysts follow this company, and institutions hold only 11% of its shares. However, if you're looking for a profitable high yielder poised for growth from rising energy prices, this is a name you should know.

The stock I'm talking about is Dorchester Minerals (Nasdaq: DMLP), an energy MLP formed in 2003 through a merger of three smaller companies. Dorchester generates revenue from royalties it collects from the oil and gas wells on its properties, which total 3 million acres spread across 25 states. Dorchester has exposure to many of North America's most prolific gas fields, including the Fayetteville Shale, the Bakken formation, the Appalachian Basin, the Barnett Shale, the Permian Basin and the Granite Wash.

Perhaps best of all, only about 30% of Dorchester's holdings are developed. That adds to the potential for a rising income stream as new wells are drilled. Unlike conventional oil and gas drillers, Dorchester has no exposure to the costs and risks of exploration, development and production. Instead, the company collects a royalty based on the sales volume of each well after the driller recoups 150% of well expenses because royalty payments are directly affected by the selling price of natural gas.

Dorchester generates more cash flow when natural gas prices are rising. Dorchester also differs from many of its MLP peers in that its general partner's fee is fixed at 4%. There are no distribution rights or incentives that increase the general partner's percentage on higher profits. Dorchester unit holders can count on consistently collecting 96% of the MLP's cash flow.

The improving outlook for natural gas demand and prices means this may be an especially good time to own Dorchester. Futures prices for natural gas surged to a 20-month high in April in response to an unusually cold spring that drained stockpiles. This prompted Goldman Sachs to raise its outlook for 2013 natural gas prices by 17%.

Natural gas accounts for roughly 75% of its reserves. Historically, Dorchester has been able to offset production declines from a steady stream of new wells on its acreage. During 2012, 490 new wells were completed on the MLP's properties.

Despite low natural gas prices that led to reduced drilling activity in many of the company's producing areas, Dorchester produced respectable results in 2012. Revenue fell 9% from a year earlier to $63.2 million, but that was still the second-highest in four years. Net income was $38 million or $1.20 a share, down only 10% from a year earlier. Despite its reduced earnings, Dorchester's cash flow actually improved 2% in 2012 to $56.4 million from a year earlier, and the MLP paid distributions of $1.79 a share to unit holders, an 8% increase over 2011.

Dorchester ended 2012 with cash of $13.8 million and no long-term debt. In fact, the company's charter precludes Dorchester from taking on long-term debt. But even without the benefit of leverage, Dorchester has been able to consistently produce returns that exceed its industry peers. In the past five years, Dorchester's operating margins have averaged 62%, which is more than four times the average 15% margin of its industry competitors. Dorchester's five-year average return on assets is 28%, nearly three times its peer group average of 10%.

Company insiders show their confidence in Dorchester's future prospects by owning a healthy 9% of shares. Another sign of management's confidence is a 3.5% increase in the distribution, to 45 cents a share. Since 2009, Dorchester has increased its annualized distribution 19%. Consensus analyst estimates forecast 5% earnings growth for Dorchester's industry peers this year, accelerating to 6% next year. I think it's likely that Dorchester can beat that estimate, thanks to its unhedged exposure to further increases in natural gas prices.

Risks to consider: Dorchester typically pays out 87% of operating cash flow as distributions. However, the amount may fluctuate due to the volatility of natural gas prices. For example, Dorchester's distributions dipped from $2.80 in 2008 to $1.50 in 2009 before rising to $1.65 in 2010 and $1.79 in 2012. Some income investors may find the variability of Dorchester's distribution too risky.

Action to take --> Dorchester is an appealing stock for investors who want generous income and exposure to rising energy prices. I like this MLP because of its industry-leading profitability, low-risk profile, significant land holdings and untapped reserves.

MLPs, thanks to their unique corporate structure, can create a headache at tax time. Each MLP issues a K-1 tax form at year end, and if you own a half-dozen of them, then that's a lot of paperwork to sort out. Yet there's a simpler way. Instead of constantly searching for the most attractive MLPs, why not keep it simple and own an investment that does all the tax work for you?

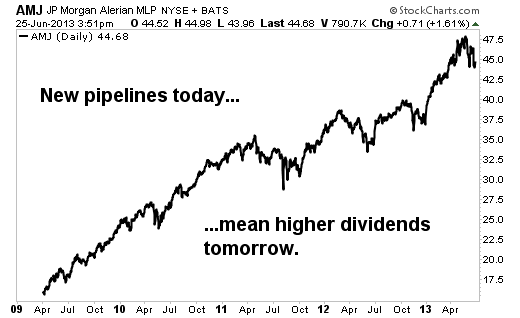

The JPMorgan Alerian MLP Index ETN (NYSE: AMJ) does just that. This is an exchange-traded note (ETN), not an exchange-traded fund (ETF), but the distinction doesn't really matter (unless the ETN issuer defaults on that note, which has never happened, as far as we know). Yet it's the ETN tax structure that saves you headaches during tax time. JPMorgan Chase (NYSE: JPM) actually owns the stocks in this ETN, and you simply invest in JPMorgan's debt instrument. At tax time, there's no K-1 to worry about. Moreover, if this ETN were structured as an ETF, it would generate corporate taxes, which would take a roughly 5% bite out of profits.

Yet the greatest appeal of this ETN is its rock-steady performance. Year after year, it rises in value as more pipelines get built and higher industry dividends are paid out. In fact, this note has risen an average of 20% over the past three years while generating below-average risk. That's why Morningstar gives this note five stars.

Despite low natural gas prices that led to reduced drilling activity in many of the company's producing areas, Dorchester produced respectable results in 2012. Revenue fell 9% from a year earlier to $63.2 million, but that was still the second-highest in four years. Net income was $38 million or $1.20 a share, down only 10% from a year earlier. Despite its reduced earnings, Dorchester's cash flow actually improved 2% in 2012 to $56.4 million from a year earlier, and the MLP paid distributions of $1.79 a share to unit holders, an 8% increase over 2011.

Dorchester ended 2012 with cash of $13.8 million and no long-term debt. In fact, the company's charter precludes Dorchester from taking on long-term debt. But even without the benefit of leverage, Dorchester has been able to consistently produce returns that exceed its industry peers. In the past five years, Dorchester's operating margins have averaged 62%, which is more than four times the average 15% margin of its industry competitors. Dorchester's five-year average return on assets is 28%, nearly three times its peer group average of 10%.

Company insiders show their confidence in Dorchester's future prospects by owning a healthy 9% of shares. Another sign of management's confidence is a 3.5% increase in the distribution, to 45 cents a share. Since 2009, Dorchester has increased its annualized distribution 19%. Consensus analyst estimates forecast 5% earnings growth for Dorchester's industry peers this year, accelerating to 6% next year. I think it's likely that Dorchester can beat that estimate, thanks to its unhedged exposure to further increases in natural gas prices.

Risks to consider: Dorchester typically pays out 87% of operating cash flow as distributions. However, the amount may fluctuate due to the volatility of natural gas prices. For example, Dorchester's distributions dipped from $2.80 in 2008 to $1.50 in 2009 before rising to $1.65 in 2010 and $1.79 in 2012. Some income investors may find the variability of Dorchester's distribution too risky.

Action to take --> Dorchester is an appealing stock for investors who want generous income and exposure to rising energy prices. I like this MLP because of its industry-leading profitability, low-risk profile, significant land holdings and untapped reserves.

MLPs, thanks to their unique corporate structure, can create a headache at tax time. Each MLP issues a K-1 tax form at year end, and if you own a half-dozen of them, then that's a lot of paperwork to sort out. Yet there's a simpler way. Instead of constantly searching for the most attractive MLPs, why not keep it simple and own an investment that does all the tax work for you?

The JPMorgan Alerian MLP Index ETN (NYSE: AMJ) does just that. This is an exchange-traded note (ETN), not an exchange-traded fund (ETF), but the distinction doesn't really matter (unless the ETN issuer defaults on that note, which has never happened, as far as we know). Yet it's the ETN tax structure that saves you headaches during tax time. JPMorgan Chase (NYSE: JPM) actually owns the stocks in this ETN, and you simply invest in JPMorgan's debt instrument. At tax time, there's no K-1 to worry about. Moreover, if this ETN were structured as an ETF, it would generate corporate taxes, which would take a roughly 5% bite out of profits.

Yet the greatest appeal of this ETN is its rock-steady performance. Year after year, it rises in value as more pipelines get built and higher industry dividends are paid out. In fact, this note has risen an average of 20% over the past three years while generating below-average risk. That's why Morningstar gives this note five stars.

Indeed, we've discovered over time that these MLPs not only deliver solid share price gains, but also deliver more robust yields when compared with other yield-focused asset classes. According to Bloomberg, the average bond ETF yields 2.16%, the average utilities ETF yields 3.52%, and the typical REIT ETF sports a 3.55% yield. In contrast, the Alerian MLP ETN's yield currently exceeds 4.5%.

To be sure, the note has a few drawbacks, starting with a 0.85% expense ratio. Thankfully, the 20% annualized gains have made that expense load bearable, but if annual returns are smaller in the future, then those expenses will take a seemingly deeper bite. Also, like all yield plays, shares may suffer if interest rates keep rising and investors pivot back to fixed-income investments. Indeed, this ETN is off nearly 7% in the past month as interest rates have risen. Yet a still-slow U.S. economy is likely to cap further interest rate increases in the near term.

Risks to Consider: You can probably find MLPs with greater yields if you are willing to dig more deeply, but understand that higher yields signal less safety.

Action to Take --> The Alerian MLP ETN offers a compelling combination of share price appreciation, rock-solid yields and very low risk.

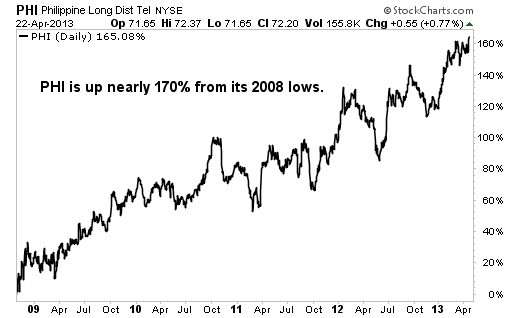

The Philippines has been transitioning from an agricultural economy to one more focused on services and manufacturing. Its political stability, youthful workforce and prevalence of English are ideal for companies already setting up business process outsourcing centers there. And the trend isn't slowing down. One of my favorite plays in this country is a high-yielding telecommunications company, PLDT (NYSE: PHI).

Established in 1928, the Philippine Long Distance Telephone Co. is the largest telecom in the Philippines and one of its largest and most traded stocks. The company has been strong in recent years, increasing revenues annually. Its policy is to declare a regular dividend of 70% of core earnings per share and a special dividend whenever possible. It has EBITDA margins of 46%, a price-to-earnings ratio of 17 and a cash dividend yield of 5%. PLDT has three operating segments: wireless, fixed line, and Internet and communications technology.

Nearly 60% of the Philippines' population owns cellphones, and the wireless segment is PLDT's core business. A 10% increase in wireless subscribers brought its share of the country's mobile market to 68% at the end of 2012. The company's wireless revenues grew at an industry-leading 15% during the year. PLDT's fixed-line division focuses on data and other network services, as well as information and communications infrastructure and services for Internet applications.

The company's Internet and communications technology division has focused on business process outsourcing and communications infrastructure; it also provides services for Internet applications and multimedia content delivery In its most recent quarter, the company reported adjusted net income of $189 million, with operating cash flow increasing to $646 million. Gross profits increased to $3.4 billion from $3 billion in 2011, and net income was up 20%, to $862 million.

To be sure, the note has a few drawbacks, starting with a 0.85% expense ratio. Thankfully, the 20% annualized gains have made that expense load bearable, but if annual returns are smaller in the future, then those expenses will take a seemingly deeper bite. Also, like all yield plays, shares may suffer if interest rates keep rising and investors pivot back to fixed-income investments. Indeed, this ETN is off nearly 7% in the past month as interest rates have risen. Yet a still-slow U.S. economy is likely to cap further interest rate increases in the near term.

Risks to Consider: You can probably find MLPs with greater yields if you are willing to dig more deeply, but understand that higher yields signal less safety.

Action to Take --> The Alerian MLP ETN offers a compelling combination of share price appreciation, rock-solid yields and very low risk.

The Philippines has been transitioning from an agricultural economy to one more focused on services and manufacturing. Its political stability, youthful workforce and prevalence of English are ideal for companies already setting up business process outsourcing centers there. And the trend isn't slowing down. One of my favorite plays in this country is a high-yielding telecommunications company, PLDT (NYSE: PHI).

Established in 1928, the Philippine Long Distance Telephone Co. is the largest telecom in the Philippines and one of its largest and most traded stocks. The company has been strong in recent years, increasing revenues annually. Its policy is to declare a regular dividend of 70% of core earnings per share and a special dividend whenever possible. It has EBITDA margins of 46%, a price-to-earnings ratio of 17 and a cash dividend yield of 5%. PLDT has three operating segments: wireless, fixed line, and Internet and communications technology.

Nearly 60% of the Philippines' population owns cellphones, and the wireless segment is PLDT's core business. A 10% increase in wireless subscribers brought its share of the country's mobile market to 68% at the end of 2012. The company's wireless revenues grew at an industry-leading 15% during the year. PLDT's fixed-line division focuses on data and other network services, as well as information and communications infrastructure and services for Internet applications.

The company's Internet and communications technology division has focused on business process outsourcing and communications infrastructure; it also provides services for Internet applications and multimedia content delivery In its most recent quarter, the company reported adjusted net income of $189 million, with operating cash flow increasing to $646 million. Gross profits increased to $3.4 billion from $3 billion in 2011, and net income was up 20%, to $862 million.

Risks to Consider: Foreign exchange risk is at play with international stocks, and currency fluctuations could impact returns. With 88% of its debt priced in U.S. dollars, depreciation against the peso could impair profitability because of higher interest payments. With 50 million mobile phone subscribers in the Philippines, the market is approaching maturity. As a result, the company's growth will come to a screeching halt unless it stays innovative.

Action to Take --> With a solid, growing dividend of 5%, PLDT is a good buy up to $75. This stock has seen tremendous growth in the past decade, and I think the best is yet to come. A gain of more than 25% in the next 12 months wouldn't surprise me.

I hope that you will take these recommendations to heart and climb aboard the dividend train to a prosperous future and a millionaire lifestyle.

Action to Take --> With a solid, growing dividend of 5%, PLDT is a good buy up to $75. This stock has seen tremendous growth in the past decade, and I think the best is yet to come. A gain of more than 25% in the next 12 months wouldn't surprise me.

I hope that you will take these recommendations to heart and climb aboard the dividend train to a prosperous future and a millionaire lifestyle.

RICH & HAPPY!

RSS Feed

RSS Feed