| MARKET CONDITIONS Overall, spinoffs have historically outperformed their parent companies. Management typically learn from their mistakes and put more conservative types in place to run the spinoffs. Some MLP spinoffs are perfect examples of this. Consider investing in spinoffs and subsidiaries as hedges against their blue chip parents. |

PM By Marshall Hargrave

There's no such thing as a free lunch, but spinoff companies are as close to free as you can get. When a company is spun off, there's a high level of forced selling. One of the best ways to think about spinoffs: "There's a natural constituency of sellers and not a natural constituency of buyers," according to "Margin of Safety" author and hedge fund manager Seth Klarman.

Simply, many shareholders who own shares of the parent company are not interested in owning the spinoff. This can be for a variety of reasons, such as different business fundamentals, weak management, or negative cash flow. In most cases, investors are selling the company for no good reason. While on the other side, the buyers are limited, as the market is inefficient in digesting data on new spinoff companies.

Spinoffs Versus The Market

Yet, over the long term, spinoff investing tends to outperform the broader market. This is not new information. A 1993 study titled "Restructuring Through Spinoffs" found that spinoff companies outperformed the S&P 500 index by 30% on average during their first three years. A similar study by Lehman Brothers concluded that between 2000 and 2005, spinoff companies outperformed the market by a whopping 45% during their first two years. JPMorgan Chase (NYSE: JPM) came to similar conclusions, finding that spinoffs outpaced the market by 20% during their first year and a half between 1985 and 1995.

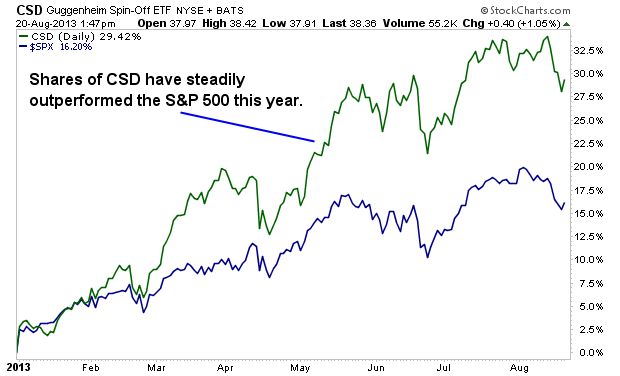

So far this year, spinoff companies have maintained that standard. The Guggenheim Spin-Off (NYSE: CSD) exchange-traded fund is up 30% this year, compared with the S&P 500's 16.5%.

There's no such thing as a free lunch, but spinoff companies are as close to free as you can get. When a company is spun off, there's a high level of forced selling. One of the best ways to think about spinoffs: "There's a natural constituency of sellers and not a natural constituency of buyers," according to "Margin of Safety" author and hedge fund manager Seth Klarman.

Simply, many shareholders who own shares of the parent company are not interested in owning the spinoff. This can be for a variety of reasons, such as different business fundamentals, weak management, or negative cash flow. In most cases, investors are selling the company for no good reason. While on the other side, the buyers are limited, as the market is inefficient in digesting data on new spinoff companies.

Spinoffs Versus The Market

Yet, over the long term, spinoff investing tends to outperform the broader market. This is not new information. A 1993 study titled "Restructuring Through Spinoffs" found that spinoff companies outperformed the S&P 500 index by 30% on average during their first three years. A similar study by Lehman Brothers concluded that between 2000 and 2005, spinoff companies outperformed the market by a whopping 45% during their first two years. JPMorgan Chase (NYSE: JPM) came to similar conclusions, finding that spinoffs outpaced the market by 20% during their first year and a half between 1985 and 1995.

So far this year, spinoff companies have maintained that standard. The Guggenheim Spin-Off (NYSE: CSD) exchange-traded fund is up 30% this year, compared with the S&P 500's 16.5%.

Earlier this year, Abbott Laboratories (NYSE: ABT) completed a split after realizing the company had grown into two distinct units. AbbVie (NYSE: ABBV) now trades as the former pharma business of Abbott Labs, while Abbott continues as a health care products and medical devices company.

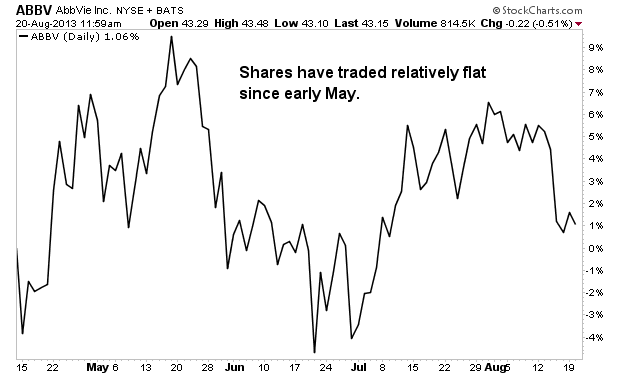

The idea of breaking up the health care and pharma businesses was to make the companies easier to value. However, it appears the market has gotten this one wrong. Spinoffs are great ways to fix mistakes. As a result, spinoffs generally have weak management, lower margins, lower returns on equity, or negative earnings. This is not the case with AbbVie. The stock had a nice run out of the gate, but interest and trading volume have since cooled off.

The idea of breaking up the health care and pharma businesses was to make the companies easier to value. However, it appears the market has gotten this one wrong. Spinoffs are great ways to fix mistakes. As a result, spinoffs generally have weak management, lower margins, lower returns on equity, or negative earnings. This is not the case with AbbVie. The stock had a nice run out of the gate, but interest and trading volume have since cooled off.

But investors should give AbbVie another look. Sometimes the market fundamentally misunderstands spinoffs. In this case, the market is treating AbbVie like a typical problematic spinoff -- but in reality, AbbVie appears more fundamentally sound than Abbott itself.

Breaking Down The Numbers

AbbVie is trading with a price-to-earnings (P/E) ratio of 13, which is well below Abbott's 60. AbbVie has an impressive 33% operating margin for the past 12 months, compared with Abbott's 20%. Abbvie is also churning out a return on capital employed (ROCE, equal to operating income divided by capital employed) of 43.5%, compared with Abbott's 21.6%.

While the companies' business models are debatable, there's no denying the strength of AbbVie's cash position and dividend yield. AbbVie has $5.50 in cash per share, which covers 12% of the share price, and the company generated $4 per share in cash flow from operations over the trailing 12 months.

AbbVie has a solid 3.6% dividend yield, which is in line with (and in most cases above) other major pharma companies and dwarfs the 1.6% yield of Abbott, its former parent. Yet unlike some of its peers, AbbVie's dividend payout (as a percentage of earnings) is below 50%. AbbVie's board has also authorized a $1.5 billion share buyback program, representing just over 2% of shares outstanding.

What About The Business?

AbbVie's key drug is Humira, an anti-inflammatory product used primarily for rheumatoid arthritis. In 2012, Humira accounted for around half of AbbVie's $18.4 billion pro forma revenues. Last year, the drug accounted for about 50% of the market for rheumatoid arthritis drugs, which is expected grow to more than $25 billion in 2017, up nearly 40% from 2012.

One concern is the fact that Humira will lose patent protection in 2016 in the United States and in 2018 in Europe. However, AbbVie's total research and development (R&D) pipeline has more than 20 compounds in Phase II or Phase III development, including five key products planned for launch before 2016.

Humira is also approved for a number of other uses, which includes HIV, Crohn's disease, psoriatic arthritis and several other ailments. These uses and the drugs in AbbVie's pipeline should help AbbVie offset any fall-off in Humira revenues.

AbbVie, which gets more than half its revenue from outside North America, has a number of growth opportunities in the U.S. and internationally. Emerging markets should see tailwinds from increased spending on health care, and in the U.S., the Affordable Care Act (aka Obamacare) is expected to provide coverage for more than 30 million uninsured Americans next year. All in all, the company has company- and industry-specific tailwinds for which the market appears to be mispricing ABBV.

Risks to consider: As with any pharma company, there are risks that patents will be challenged or the company will fail to produce new revenue-generating products. AbbVie faces patent expirations for its top drug Humira in the next several years, which could be a negative if its other products fail to come to market in a timely fashion.

Action to take --> Consider buying shares of AbbVie, which has a well-developed R&D pipeline and a cheap valuation. With just a modest 20 times P/E multiple on AbbVie management's 2013 EPS forecast of $3.10, the stock should trade north of $60. Its solid cash position and robust dividend also give the stock some downside protection.

Breaking Down The Numbers

AbbVie is trading with a price-to-earnings (P/E) ratio of 13, which is well below Abbott's 60. AbbVie has an impressive 33% operating margin for the past 12 months, compared with Abbott's 20%. Abbvie is also churning out a return on capital employed (ROCE, equal to operating income divided by capital employed) of 43.5%, compared with Abbott's 21.6%.

While the companies' business models are debatable, there's no denying the strength of AbbVie's cash position and dividend yield. AbbVie has $5.50 in cash per share, which covers 12% of the share price, and the company generated $4 per share in cash flow from operations over the trailing 12 months.

AbbVie has a solid 3.6% dividend yield, which is in line with (and in most cases above) other major pharma companies and dwarfs the 1.6% yield of Abbott, its former parent. Yet unlike some of its peers, AbbVie's dividend payout (as a percentage of earnings) is below 50%. AbbVie's board has also authorized a $1.5 billion share buyback program, representing just over 2% of shares outstanding.

What About The Business?

AbbVie's key drug is Humira, an anti-inflammatory product used primarily for rheumatoid arthritis. In 2012, Humira accounted for around half of AbbVie's $18.4 billion pro forma revenues. Last year, the drug accounted for about 50% of the market for rheumatoid arthritis drugs, which is expected grow to more than $25 billion in 2017, up nearly 40% from 2012.

One concern is the fact that Humira will lose patent protection in 2016 in the United States and in 2018 in Europe. However, AbbVie's total research and development (R&D) pipeline has more than 20 compounds in Phase II or Phase III development, including five key products planned for launch before 2016.

Humira is also approved for a number of other uses, which includes HIV, Crohn's disease, psoriatic arthritis and several other ailments. These uses and the drugs in AbbVie's pipeline should help AbbVie offset any fall-off in Humira revenues.

AbbVie, which gets more than half its revenue from outside North America, has a number of growth opportunities in the U.S. and internationally. Emerging markets should see tailwinds from increased spending on health care, and in the U.S., the Affordable Care Act (aka Obamacare) is expected to provide coverage for more than 30 million uninsured Americans next year. All in all, the company has company- and industry-specific tailwinds for which the market appears to be mispricing ABBV.

Risks to consider: As with any pharma company, there are risks that patents will be challenged or the company will fail to produce new revenue-generating products. AbbVie faces patent expirations for its top drug Humira in the next several years, which could be a negative if its other products fail to come to market in a timely fashion.

Action to take --> Consider buying shares of AbbVie, which has a well-developed R&D pipeline and a cheap valuation. With just a modest 20 times P/E multiple on AbbVie management's 2013 EPS forecast of $3.10, the stock should trade north of $60. Its solid cash position and robust dividend also give the stock some downside protection.

RSS Feed

RSS Feed