| MARKET CONDITIONS This is the second time I've mentioned this franchise. There's a reason... DNKN is prime to take a few premiums. I'm not giving you the details on how the option play would work on this one but you need to think in terms of pillaging the opportunity. |

If you live in New England, the orange-and-purple Dunkin' Donuts logo seems to appear at every turn. Operated by parent company Dunkin' Brands Group (NASDAQ: DNKN), the quick-serve restaurant chain is a regional institution that's almost as beloved as the Boston Red Sox.

But make no mistake: Dunkin' Donuts is rapidly pushing its presence beyond the environs of Beantown.

Based in Canton, Mass., Dunkin' Brands currently operates 10,600 Dunkin' Donuts restaurants and 7,000 Baskin-Robbins restaurants in 60 countries. The company is now unfurling its flagship Dunkin' Donuts brand from coast to coast in the US, with plans to increase the number of doughnut shops in the country to about 15,000 over the next two decades.

Despite health concerns about fast food and the national obsession with dieting, Americans still love their doughnuts and coffee. In the US alone, more than 10 billion donuts are made every year, generating about $3.6 billion in annual revenue.

Dunkin' Donuts is the world's largest operator of doughnut shops but it's number two in the overall coffee and snack-shop market, with roughly 23 percent of global market share, according to industry research firm IBISWorld. Its biggest competitor, Starbucks (NASDAQ: SBUX), is number one with roughly 32.6 percent. Dunkin' Donuts is now placing Starbucks in its sights.

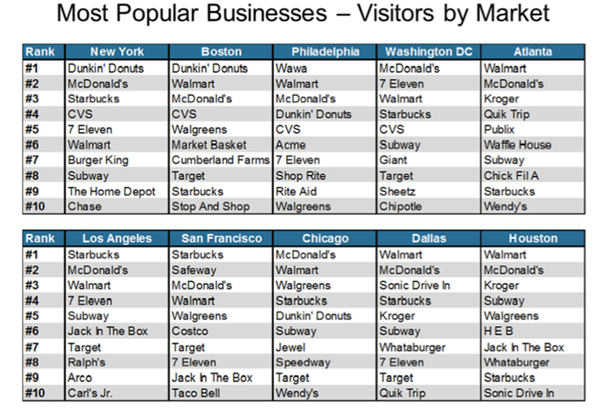

According to Placed, a consumer behavior research firm, Dunkin' Donuts currently dominates the heavily populated Boston-New York City-Philadelphia corridor, but it badly lags competitors in other major metropolitan markets (see table below).

But make no mistake: Dunkin' Donuts is rapidly pushing its presence beyond the environs of Beantown.

Based in Canton, Mass., Dunkin' Brands currently operates 10,600 Dunkin' Donuts restaurants and 7,000 Baskin-Robbins restaurants in 60 countries. The company is now unfurling its flagship Dunkin' Donuts brand from coast to coast in the US, with plans to increase the number of doughnut shops in the country to about 15,000 over the next two decades.

Despite health concerns about fast food and the national obsession with dieting, Americans still love their doughnuts and coffee. In the US alone, more than 10 billion donuts are made every year, generating about $3.6 billion in annual revenue.

Dunkin' Donuts is the world's largest operator of doughnut shops but it's number two in the overall coffee and snack-shop market, with roughly 23 percent of global market share, according to industry research firm IBISWorld. Its biggest competitor, Starbucks (NASDAQ: SBUX), is number one with roughly 32.6 percent. Dunkin' Donuts is now placing Starbucks in its sights.

According to Placed, a consumer behavior research firm, Dunkin' Donuts currently dominates the heavily populated Boston-New York City-Philadelphia corridor, but it badly lags competitors in other major metropolitan markets (see table below).

Dunkin' Brands' concentration in the Northeast is a limitation but also a great advantage—it gives the company huge opportunities for growth in the rest of the US, especially the West Coast.

Filling the Holes

Amazingly, the company operates no outlets in California, but that vast geographical hole is getting filled. In July, Dunkin' Donuts announced a deal with four franchise groups to open 45 restaurants in the Golden State in 2015.

Other under-represented states are in line. In August, Dunkin' Donuts inked an agreement with an existing franchise group, Sizzling Donuts, LLC, to develop 18 traditional Dunkin' Donut restaurants and one Dunkin' Donuts/Baskin-Robbins combination location in communities throughout southern Texas. The first restaurant is slated to open in 2014 and the remainder by 2018.

Also in August, Dunkin' Donuts signed a development deal with its franchise partner, Travel Mart, to set up 7 new units in La Crosse and Eau Claire, Wisconsin.

Travel Mart is a retailer of fuel and food products in convenience stores; the first of these new Dunkin' locations in Wisconsin are scheduled to open in 2014, with the rest by 2020.

Dunkin' Brands' expansion is facilitated by the company's business model: 100 percent of its stores are opened as franchises, which keeps a lid on capital costs. In 2012, the company incurred capital expenditures of only $23.4 million, a modest sum considering the high number of new location launches.

Small wonder, then, that shares of Dunkin' Brands have outpaced the broader market, soaring by more than 30 percent so far this year, as the global economic recovery accelerates and consumers increasingly hanker for the company's doughnuts, coffee, flavored beverages, and specialty sandwiches.

To borrow the company's advertising slogan, investors seem to run on Dunkin' (see stock price graph below).

Filling the Holes

Amazingly, the company operates no outlets in California, but that vast geographical hole is getting filled. In July, Dunkin' Donuts announced a deal with four franchise groups to open 45 restaurants in the Golden State in 2015.

Other under-represented states are in line. In August, Dunkin' Donuts inked an agreement with an existing franchise group, Sizzling Donuts, LLC, to develop 18 traditional Dunkin' Donut restaurants and one Dunkin' Donuts/Baskin-Robbins combination location in communities throughout southern Texas. The first restaurant is slated to open in 2014 and the remainder by 2018.

Also in August, Dunkin' Donuts signed a development deal with its franchise partner, Travel Mart, to set up 7 new units in La Crosse and Eau Claire, Wisconsin.

Travel Mart is a retailer of fuel and food products in convenience stores; the first of these new Dunkin' locations in Wisconsin are scheduled to open in 2014, with the rest by 2020.

Dunkin' Brands' expansion is facilitated by the company's business model: 100 percent of its stores are opened as franchises, which keeps a lid on capital costs. In 2012, the company incurred capital expenditures of only $23.4 million, a modest sum considering the high number of new location launches.

Small wonder, then, that shares of Dunkin' Brands have outpaced the broader market, soaring by more than 30 percent so far this year, as the global economic recovery accelerates and consumers increasingly hanker for the company's doughnuts, coffee, flavored beverages, and specialty sandwiches.

To borrow the company's advertising slogan, investors seem to run on Dunkin' (see stock price graph below).

Most of Dunkin' Donuts' customers visit for a quick stop in the morning, but the chain is trying to alter those traffic patterns with the addition of new sandwiches and bakery items suitable for all times of the day. The goal is to attract the business luncheon crowd that's willing to sit longer and spend more.

This year, Dunkin' Donuts expanded its menu by 30 items, with more elaborate fare such as roast beef, turkey sausage and steak sandwiches, as well as tuna and chicken salad wraps. The menu also is featuring more gluten-free items, for the growing ranks of "gluten intolerant” customers.

Dunkin' Brands is pursuing a two-pronged attack designed to attract customers from both ends of the spectrum—those on the run who want to grab a baked treat and a jolt of caffeine, as well as those with the time and inclination to sit down and enjoy a fuller (and higher margin) meal.

Dunkin' Donuts is renovating its existing outlets to closely resemble the more-upscale ambiance of Starbucks, giving the coffee juggernaut a run for its money.

Dunkin' Donuts familiar, vividly hued signage is staying the same, but the interiors of its restaurants are adopting earth tones and padded leather furniture for a cozier café feel. At the same time, capital expenditures remain under control, giving the chain a financial edge over Starbucks. In the second quarter, Dunkin' Brands reported an operating margin of 42.1 percent, compared to 16.4 percent for Starbucks.

Dunkin' Donuts also has introduced non-doughnut breakfast items such as bagels and cream cheese, to stave off not just Starbucks but other competitors such as Tim Hortons (NYSE: THI).

What's more, Dunkin' Donuts is expanding into smaller, non-conventional locations, such as truck and car plazas along highways, subway and bus stops, college campuses, supermarkets, sports arenas, amusement parks, and even military bases.

Sweet Operating Results

In the second quarter, Dunkin' Brands franchisees opened 151 new Dunkin' Donuts and Baskin-Robbins restaurants around the globe, including 63 new Dunkin' Donuts locations in the US and 33 overseas.

So far, Dunkin' Brands' strategic expansion is bringing in the dough. Dunkin' Brands' second-quarter revenue came in at $182.5 million, an increase of 5.9 percent compared to the same period a year ago, largely from higher royalty income.

Second-quarter earnings reached $40.8 million compared to $18.5 million in the same year-ago quarter, for a whopping year-over-year increase of 120.6 percent. Earnings per share (EPS) increased year-over-year by 24.2 percent to $0.41.

For the full year, management projects EPS of between $1.50-$1.53, in line with analysts' expectations.

In the second quarter, Dunkin' Brands also bought back 400,000 shares. At the end of the quarter, shares worth about $33 million remained under the company's existing share repurchase plan.

In contrast to Dunkin' Brands' US-oriented expansion, chief rival Krispy Kreme Doughnuts (NYSE: KKD) is intent on adding outlets overseas, a focus that's riskier because of higher capital costs as well as the recent emerging market slump.

Moreover, Krispy Kreme's stock valuation appears to be in the throes of a sugar high, with a trailing 12-month price-to-earnings (P/E) ratio of 58.8, compared to Dunkin' Brands' trailing P/E of 36.6.

Even Dunkin' Brands' P/E seems a bit pricey, compared to the trailing P/E of 21.8 for its industry of restaurants. However, the stock's valuation is reasonable in the context of Wall Street's projection of 16 percent EPS growth for the company in 2013. As denizens of the company's home turf might say, Dunkin' Brands' long-term prospects look "wicked good.”

This year, Dunkin' Donuts expanded its menu by 30 items, with more elaborate fare such as roast beef, turkey sausage and steak sandwiches, as well as tuna and chicken salad wraps. The menu also is featuring more gluten-free items, for the growing ranks of "gluten intolerant” customers.

Dunkin' Brands is pursuing a two-pronged attack designed to attract customers from both ends of the spectrum—those on the run who want to grab a baked treat and a jolt of caffeine, as well as those with the time and inclination to sit down and enjoy a fuller (and higher margin) meal.

Dunkin' Donuts is renovating its existing outlets to closely resemble the more-upscale ambiance of Starbucks, giving the coffee juggernaut a run for its money.

Dunkin' Donuts familiar, vividly hued signage is staying the same, but the interiors of its restaurants are adopting earth tones and padded leather furniture for a cozier café feel. At the same time, capital expenditures remain under control, giving the chain a financial edge over Starbucks. In the second quarter, Dunkin' Brands reported an operating margin of 42.1 percent, compared to 16.4 percent for Starbucks.

Dunkin' Donuts also has introduced non-doughnut breakfast items such as bagels and cream cheese, to stave off not just Starbucks but other competitors such as Tim Hortons (NYSE: THI).

What's more, Dunkin' Donuts is expanding into smaller, non-conventional locations, such as truck and car plazas along highways, subway and bus stops, college campuses, supermarkets, sports arenas, amusement parks, and even military bases.

Sweet Operating Results

In the second quarter, Dunkin' Brands franchisees opened 151 new Dunkin' Donuts and Baskin-Robbins restaurants around the globe, including 63 new Dunkin' Donuts locations in the US and 33 overseas.

So far, Dunkin' Brands' strategic expansion is bringing in the dough. Dunkin' Brands' second-quarter revenue came in at $182.5 million, an increase of 5.9 percent compared to the same period a year ago, largely from higher royalty income.

Second-quarter earnings reached $40.8 million compared to $18.5 million in the same year-ago quarter, for a whopping year-over-year increase of 120.6 percent. Earnings per share (EPS) increased year-over-year by 24.2 percent to $0.41.

For the full year, management projects EPS of between $1.50-$1.53, in line with analysts' expectations.

In the second quarter, Dunkin' Brands also bought back 400,000 shares. At the end of the quarter, shares worth about $33 million remained under the company's existing share repurchase plan.

In contrast to Dunkin' Brands' US-oriented expansion, chief rival Krispy Kreme Doughnuts (NYSE: KKD) is intent on adding outlets overseas, a focus that's riskier because of higher capital costs as well as the recent emerging market slump.

Moreover, Krispy Kreme's stock valuation appears to be in the throes of a sugar high, with a trailing 12-month price-to-earnings (P/E) ratio of 58.8, compared to Dunkin' Brands' trailing P/E of 36.6.

Even Dunkin' Brands' P/E seems a bit pricey, compared to the trailing P/E of 21.8 for its industry of restaurants. However, the stock's valuation is reasonable in the context of Wall Street's projection of 16 percent EPS growth for the company in 2013. As denizens of the company's home turf might say, Dunkin' Brands' long-term prospects look "wicked good.”

RSS Feed

RSS Feed