| MARKET CONDITIONS As I regularly scan the Wall Street Journal, I sometimes come across an eye-catching headline. Merrill Lynch's recent report on agricultural equipment provider Agco (Nasdaq: AGCO) is a great example: "Margin Upside, Divy Could Soar, Raising Estimates." It's the middle part that got my attention. |

Merrill's analysts noted the dividend could be poised for a big change: "AGCO currently pays out only 7% of earnings per share (EPS) in the form of dividends. The dividend could triple in the next few years on flat EPS of $6 if the company simply goes to a 20% payout ratio."

What those analysts didn't say: Many companies pay out 40% or more of their income to dividends, which means the dividend payments could actually swell far higher than these analysts suspect.

The Revolution Is Already Underway

Have the executives at Agco been under a rock these past few years as other companies have already sharply hiked their payouts? No, they just wanted to show an extra dose of patience before making such a big move. After all, it feels as if we're not far removed from many recent global crises.

Yet Agco, like many other firms, now sees that the U.S. and Europe, which still account for half of global GDP, are proving to have increasingly resilient economies. And you can see the confidence in the form of improving financial projections: In its view of Agco, for example, Merrill Lynch foresees "further opportunity for margin expansion in coming years based on the company's numerous internal initiatives," predicting free cash flow will rise nearly 150%, to $570 million, by 2015.

Not Yet On The Radar

As Agco's dividend currently yields just 0.6%, most income-focused investors still haven't looked at this company. A tripling of the dividend would simply push the yield into respectable (but not great) territory. But what about companies that have decent yields now, but are poised for great yields in the years to come?

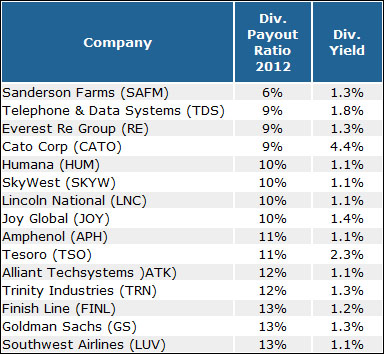

I went in search of stocks that currently yield more than 1%, but could be yielding 3%, 4% or even 5% in a few years. To find them, I focused on companies with very low payout ratios. Of all the companies in the S&P 500, 400 (mid-cap) and 600 (small cap), these are the companies with the lowest payout ratios with a current dividend yield of at least 1%.

What those analysts didn't say: Many companies pay out 40% or more of their income to dividends, which means the dividend payments could actually swell far higher than these analysts suspect.

The Revolution Is Already Underway

Have the executives at Agco been under a rock these past few years as other companies have already sharply hiked their payouts? No, they just wanted to show an extra dose of patience before making such a big move. After all, it feels as if we're not far removed from many recent global crises.

Yet Agco, like many other firms, now sees that the U.S. and Europe, which still account for half of global GDP, are proving to have increasingly resilient economies. And you can see the confidence in the form of improving financial projections: In its view of Agco, for example, Merrill Lynch foresees "further opportunity for margin expansion in coming years based on the company's numerous internal initiatives," predicting free cash flow will rise nearly 150%, to $570 million, by 2015.

Not Yet On The Radar

As Agco's dividend currently yields just 0.6%, most income-focused investors still haven't looked at this company. A tripling of the dividend would simply push the yield into respectable (but not great) territory. But what about companies that have decent yields now, but are poised for great yields in the years to come?

I went in search of stocks that currently yield more than 1%, but could be yielding 3%, 4% or even 5% in a few years. To find them, I focused on companies with very low payout ratios. Of all the companies in the S&P 500, 400 (mid-cap) and 600 (small cap), these are the companies with the lowest payout ratios with a current dividend yield of at least 1%.

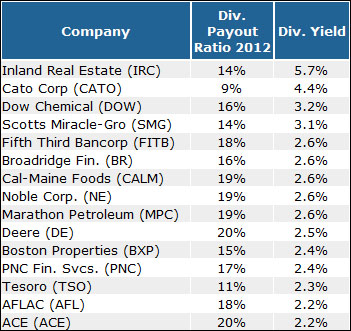

Of course, investors may want to seek out companies that already offer more appealing yields but are in a position to boost their dividends at a still-strong pace. Looking at that same group of 1,500 companies, here are the highest current yielders that have a payout ratio below 30%.

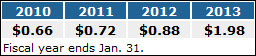

You'll notice that women's apparel retailer Cato Corp. (Nasdaq: CATO) makes both lists. The company is what we call a "Hidden High-Yielder." Go to any popular financial website, and it will appear as if Cato pays annual dividend of a paltry $0.20 a share. But looks are deceiving. Cato likes to maintain a conservative formal dividend, but often manages to slip in irregular dividend payments that can start to really add up.

In its most recent fiscal year, Cato delivered an extra $1-a-share dividend ahead of looming changes in the tax code, so don't look for a similar payout this year. But if history is any guide, future annual dividends will be a lot closer to $1 a share, and not just the $0.20 a share that many websites will tell you.

Dow Chemical (NYSE: DOW) is another example of a company positioned for robust dividend growth, thanks to an ongoing balance sheet transformation. The chemical giant had been carrying an ungainly balance sheet, as long-term total debt rose to $20.6 billion by the end of 2010.

Yet Dow now appears committed to shrinking that debt load: It's already less than $17.5 billion and should sink below $15 billion over the next two years, according to management. As debt moves to more manageable levels, look for Dow to shift its focus toward dividends. The payout has already been boosted from $0.60 a share in 2010 to a current $1.28 a share (good for a 3.3% yield).

But the smaller debt load should enable Dow Chemical to double its payout ratio in coming years, setting the stage for a dividend yield above 6% (if you lock in at today's stock prices).

Risks to Consider: We're in the midst of a steady expansion in payout ratios, but companies tend to reduce their dividends when the economy contracts, as was the case in 2008. So keep an eye on the broader economic environment in which each of these companies operates.

Action to Take --> Certain industries predominate the "low payout ratio" theme. Banks and insurers, many of which are only now sufficiently capitalized to satisfy regulators, stand to pay solid attention to their dividends in coming years. Insurers Chubb (NYSE: CB), Unum (NYSE: UNM), Assurant (NYSE: AIZ) and Protective Life (NYSE: PL), for example, all have payout ratios below 20% (and typically trade below book value as an added value kicker).

If you're in search of stocks that can offer robust dividend growth, simply calculate how much of their current earnings are geared toward the dividend. If the payout ratios are below 20%, and cash flow appears to be stable and growing, then you may be looking at some of the dividend stars of 2014.

Dow Chemical (NYSE: DOW) is another example of a company positioned for robust dividend growth, thanks to an ongoing balance sheet transformation. The chemical giant had been carrying an ungainly balance sheet, as long-term total debt rose to $20.6 billion by the end of 2010.

Yet Dow now appears committed to shrinking that debt load: It's already less than $17.5 billion and should sink below $15 billion over the next two years, according to management. As debt moves to more manageable levels, look for Dow to shift its focus toward dividends. The payout has already been boosted from $0.60 a share in 2010 to a current $1.28 a share (good for a 3.3% yield).

But the smaller debt load should enable Dow Chemical to double its payout ratio in coming years, setting the stage for a dividend yield above 6% (if you lock in at today's stock prices).

Risks to Consider: We're in the midst of a steady expansion in payout ratios, but companies tend to reduce their dividends when the economy contracts, as was the case in 2008. So keep an eye on the broader economic environment in which each of these companies operates.

Action to Take --> Certain industries predominate the "low payout ratio" theme. Banks and insurers, many of which are only now sufficiently capitalized to satisfy regulators, stand to pay solid attention to their dividends in coming years. Insurers Chubb (NYSE: CB), Unum (NYSE: UNM), Assurant (NYSE: AIZ) and Protective Life (NYSE: PL), for example, all have payout ratios below 20% (and typically trade below book value as an added value kicker).

If you're in search of stocks that can offer robust dividend growth, simply calculate how much of their current earnings are geared toward the dividend. If the payout ratios are below 20%, and cash flow appears to be stable and growing, then you may be looking at some of the dividend stars of 2014.

RSS Feed

RSS Feed