| MARKET CONDITIONS PROFILED: BuArcelorMittal (NYSE: MT) ArcelorMittal (NYSE: MT) Banco Santander Brasil (NYSE: BSBR) |

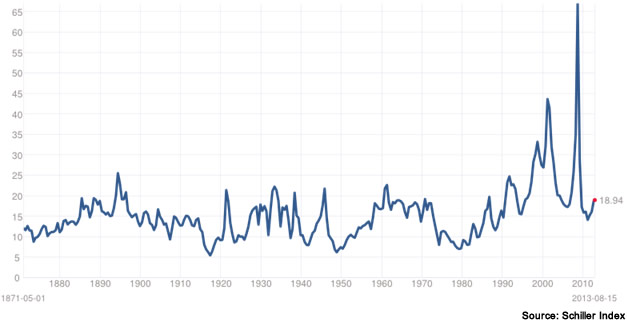

As the market reaches near record highs, it's becoming harder to find value. Historically, the average price-to-earnings (P/E) ratio of the S&P 500 is about 15. Today, the average is 19.

I'm not saying we're in a crazy bubble or the market is about to collapse. I'm only saying that stocks have gotten more expensive recently as low Treasury and savings account returns have forced investors into equities in a desperate search for yield.

You may remember May 2009 when the average P/E ratio for the S&P 500 hit an all-time high of 123 (a number that is literally off the chart below).

I'm not saying we're in a crazy bubble or the market is about to collapse. I'm only saying that stocks have gotten more expensive recently as low Treasury and savings account returns have forced investors into equities in a desperate search for yield.

You may remember May 2009 when the average P/E ratio for the S&P 500 hit an all-time high of 123 (a number that is literally off the chart below).

Of course, the P/E ratio is just one measurement of value. Others include the price/earnings-to-growth (PEG) ratio, dividend growth, earnings per share (EPS) and free cash flow.

Peter Lynch was partial to using the PEG rate to value companies. In his book, "One Up On Wall Street," Lynch wrote:

"The P/E ratio of any company that's fairly priced will equal its growth rate."

Since the equation for PEG looks like this:

Peter Lynch was partial to using the PEG rate to value companies. In his book, "One Up On Wall Street," Lynch wrote:

"The P/E ratio of any company that's fairly priced will equal its growth rate."

Since the equation for PEG looks like this:

What Lynch might term as a fairly valued company will have its PEG equal to 1.

It is a basic tenet in the Benjamin Graham value school of investing that the biggest gains are made by finding undervalued companies.

But we're not just pursuing any old undervalued company -- some stocks are in the dumps for a good reason, and we don't want to touch them with a 10-foot pole.

We're looking for companies that have been "unfairly punished" by market sentiment, have suffered temporary setbacks, and are poised for big turnarounds.

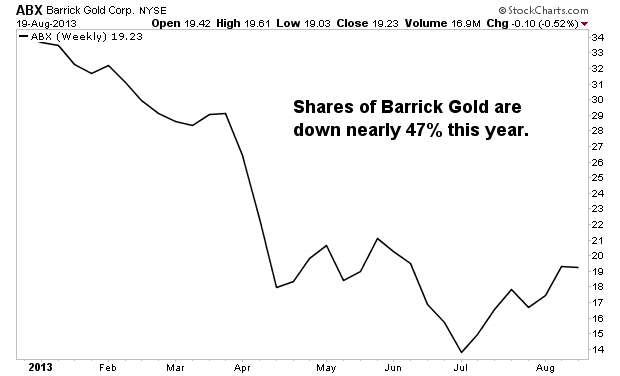

A recent example of this phenomenon is Barrick Gold (NYSE: ABX). When I wrote about Barrick a few months ago, shares were trading at its the lowest price since 2004. For the reasons I explained in that article, I thought the market had pushed Barrick into oversold territory.

I was wrong about the bottom -- Barrick continued to slide for another month. But since hitting bottom a month ago, Barrick is up 25 %, with no signs of slowing down.

It is a basic tenet in the Benjamin Graham value school of investing that the biggest gains are made by finding undervalued companies.

But we're not just pursuing any old undervalued company -- some stocks are in the dumps for a good reason, and we don't want to touch them with a 10-foot pole.

We're looking for companies that have been "unfairly punished" by market sentiment, have suffered temporary setbacks, and are poised for big turnarounds.

A recent example of this phenomenon is Barrick Gold (NYSE: ABX). When I wrote about Barrick a few months ago, shares were trading at its the lowest price since 2004. For the reasons I explained in that article, I thought the market had pushed Barrick into oversold territory.

I was wrong about the bottom -- Barrick continued to slide for another month. But since hitting bottom a month ago, Barrick is up 25 %, with no signs of slowing down.

Let's look at three stocks poised for a similar comeback.

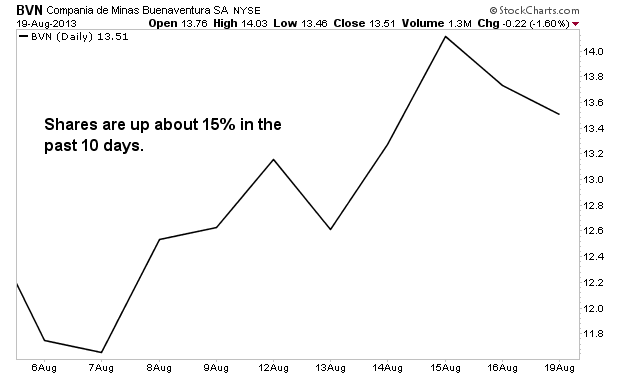

| You'd have to go back to 2005 to find share prices this low. With a forward P/E of 5, a PEG ratio just over 1, and share prices below book value, Buenaventura has seen better days. But the recent uptrend in gold prices, combined with several new projects under production, could be the catalyst the company needs to turn things around. In 2010, Buenaventura began production at its La Zanja gold mine in Peru. The mine is expected to produce 100,000 ounces of gold per year at below-average costs. The mine is operated as a joint venture with Newmont Mining (NYSE: NEM). Tantahuatay, another Peruvian gold mine with similar production estimates and costs, began production in August 2011. The company's Chucapaca project is expected to be a top-tier asset, but won't begin production for several years. |

Because its assets are located in Peru, there are geopolitical risks that come with an investment in Buenaventura. However, these risks are offset by the fact that the company has been on good terms with the country's government since the company's founding in 1953. With the sudden uptick in gold prices, Buenaventura shares have risen sharply over the past week. |

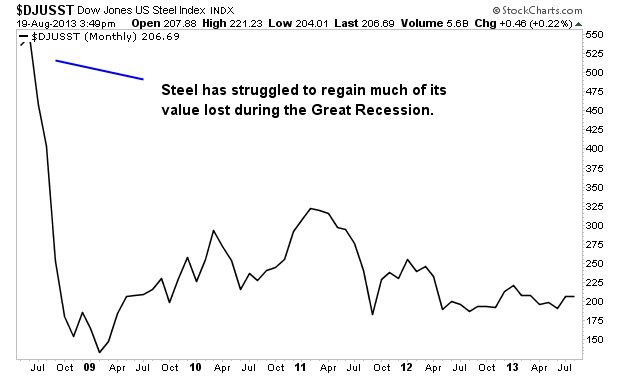

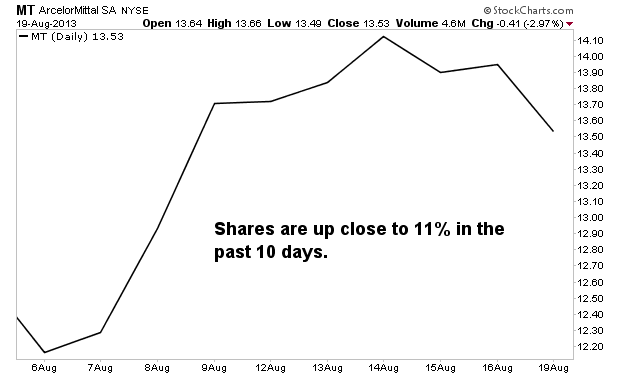

| Shares of the world's largest steel producer are are trading at its lowest price since 2004. ArcelorMittal is trading at less than half of book value with a PEG ratio of -5 and a P/E ratio of 14. Although the steel industry has been hammered by the Great Recession, there are signs of economic recovery, especially in Europe where the company is based. Emerging markets remain fertile territory for expansion. |

|

ArcelorMittal supplies 20% of automakers' steel worldwide. In emerging markets, which represent 80% of global demand, the company has been aggressive. It now boasts a 30% share of the Brazilian steel market and is fighting for an increased presence in India and China.

Although it owns minority interests in two Chinese steel producers, it will be an uphill struggle for ArcelorMittal to establish any kind of dominant role in China. China is the world's largest consumer of steel, yet the Chinese government has kept tight reins on the market and has blocked any attempts at majority holdings by foreign companies.

Although it owns minority interests in two Chinese steel producers, it will be an uphill struggle for ArcelorMittal to establish any kind of dominant role in China. China is the world's largest consumer of steel, yet the Chinese government has kept tight reins on the market and has blocked any attempts at majority holdings by foreign companies.

| It may seem crazy to recommend a Brazilian bank, even when it's trading for historically cheap prices. After all, the country has a scary history of sudden inflation and government intervention into private business. But the fact is the company generates enormous amounts of consistent free cash flow ($8 billion last year) and has paid a dividend over 3% for the past three years. Here's why BSBR could be poised for a turnaround: In Brazil, six banks control more than 90% of the banking system's assets. And of these six, BSBR is the smallest. With just 10% of the country's current market share, it has plenty of room to grow. The company is majority owned by Banco Santander (NYSE: SAN), Spain's largest bank. |

This controlling interest can be seen as a positive in the sense that BSBR has a "Rich Parent" relationship with SAN. SAN's experienced management team has provided guidance for SAN during recent acquisitions and also gives the company a leg-up when recruiting international clients. Banco Santander Brasil is currently trading at half of book value with a forward P/E of 7 and a PEG ratio just over 1. |

***Risks to Consider: All three stocks carry considerable risk, primarily due to geopolitical concerns.

Action to Take --> These companies have been around for a while, pay dividends, and at these prices, have considerable upside potential.

My favorite stock of the three is Buenaventura. I've been bullish on gold miners for a while now due to the huge disconnect between their valuations and the price of gold. The stock is currently in an uptrend and should make for a great short-term investment at recent prices.

For contrarian investors eager to buy when there's "blood in the streets," all three stocks fit the bill.

RSS Feed

RSS Feed