Amber Hestla

| MARKET CONDITIONS I love Amber Hestla's no-nonsense approach to investing. She takes the complexities out of perceptions shared by both investors and brokers when it comes to achieving realistic gains in the market... particularly with Blue Chips. I sometimes get the puppy dog gaze when I tell people that if they aren't realizing at least 18% annually then something is wrong... and that's being very conservative! You don't need a lot of money... just a lot of "know how". A precise and commonsense approach as described below will help you achieve if not surpass 18% annually. |

By Amber Hestla

For 41 weeks in a row, the options trades I've recommended to my readers have been profitable. And on average, my readers are collecting 7.5% in "Instant Income" every 48 days. So far, we're 32 for 32 when it comes to closed trades. How am I doing it? It's actually pretty simple... but it requires some investors to leave their comfort zone.

Options are one of the most misunderstood corners of the financial world. Many investors steer clear of options because they have a reputation for being risky, but that's not always the case.

My strategy involves selling options on undervalued stocks. And as we've mentioned selling "put" options is one of the most effective income strategies in the world.

But today, I want to tell you about a different strategy -- selling covered calls.

A covered call strategy involves selling call options on stocks that you own. This allows you to generate income from selling options while benefitting from the potential upside by owning the stock. The downside risk is partly reduced by the income generated from selling options, which offsets potential losses in the stock.

If you're a little confused by that, don't worry. An example of a trade you can make today should help clear things up.

Aetna (NYSE: AET) is one of the largest health insurers in the nation. It is also a value stock that is trading with a price-to-earnings (P/E) ratio of about 13, about average for its industry. Despite the average valuation, AET is expected to grow faster than other large insurers, with earnings growth expected to average 10% a year over the next five years.

As health insurance stays in the news, traders can be expected to look at companies like AET, and the stock could be volatile. That creates an opportunity for short-term gains.

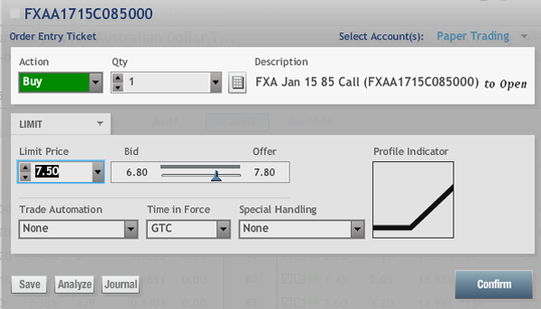

AET has recently traded around $67.75. Traders can buy 100 shares of AET and immediately sell a call option expiring in January with a strike price of $70 for about $1 per share, or $100 per contract, since each contract controls 100 shares.

A call option gives the buyer the right to buy 100 shares of stock for a predetermined price (the strike price) at any time prior to the expiration date. Call sellers have an obligation to sell the shares if the buyer exercises their right to buy the stock, which they will do if the stock price is above the strike price when the option expires.

In this case, if AET is above $70 when the call expires on Jan. 17, the buyer will exercise the option and you will have to sell your 100 shares at $70. Your profit on the trade will be equal to the difference in the sale price and the purchase price ($2.25 in this case) plus the option premium of $1 for a total of $3.25 per share. That would be a return of 4.8% in about two months, or 54 days to be exact.

If AET is below $70 in January, you will have the opportunity to sell another call option and generate additional income. The current price of the option is about 1.4% of the stock's price. Selling an option for that amount every 54 days would generate income of about 9.5% a year. AET also pays a dividend for a yield of 1.2% a year. The combined income of 10.7% a year is almost nine times as much as owning the stock alone -- that's a 790% increase in income. And this income could offset any potential losses in AET.

Covered calls, and options selling in general, are versatile strategies that can reduce risk, allow you to benefit from short-term market moves and generate income all at the same time.

For 41 weeks in a row, the options trades I've recommended to my readers have been profitable. And on average, my readers are collecting 7.5% in "Instant Income" every 48 days. So far, we're 32 for 32 when it comes to closed trades. How am I doing it? It's actually pretty simple... but it requires some investors to leave their comfort zone.

Options are one of the most misunderstood corners of the financial world. Many investors steer clear of options because they have a reputation for being risky, but that's not always the case.

My strategy involves selling options on undervalued stocks. And as we've mentioned selling "put" options is one of the most effective income strategies in the world.

But today, I want to tell you about a different strategy -- selling covered calls.

A covered call strategy involves selling call options on stocks that you own. This allows you to generate income from selling options while benefitting from the potential upside by owning the stock. The downside risk is partly reduced by the income generated from selling options, which offsets potential losses in the stock.

If you're a little confused by that, don't worry. An example of a trade you can make today should help clear things up.

Aetna (NYSE: AET) is one of the largest health insurers in the nation. It is also a value stock that is trading with a price-to-earnings (P/E) ratio of about 13, about average for its industry. Despite the average valuation, AET is expected to grow faster than other large insurers, with earnings growth expected to average 10% a year over the next five years.

As health insurance stays in the news, traders can be expected to look at companies like AET, and the stock could be volatile. That creates an opportunity for short-term gains.

AET has recently traded around $67.75. Traders can buy 100 shares of AET and immediately sell a call option expiring in January with a strike price of $70 for about $1 per share, or $100 per contract, since each contract controls 100 shares.

A call option gives the buyer the right to buy 100 shares of stock for a predetermined price (the strike price) at any time prior to the expiration date. Call sellers have an obligation to sell the shares if the buyer exercises their right to buy the stock, which they will do if the stock price is above the strike price when the option expires.

In this case, if AET is above $70 when the call expires on Jan. 17, the buyer will exercise the option and you will have to sell your 100 shares at $70. Your profit on the trade will be equal to the difference in the sale price and the purchase price ($2.25 in this case) plus the option premium of $1 for a total of $3.25 per share. That would be a return of 4.8% in about two months, or 54 days to be exact.

If AET is below $70 in January, you will have the opportunity to sell another call option and generate additional income. The current price of the option is about 1.4% of the stock's price. Selling an option for that amount every 54 days would generate income of about 9.5% a year. AET also pays a dividend for a yield of 1.2% a year. The combined income of 10.7% a year is almost nine times as much as owning the stock alone -- that's a 790% increase in income. And this income could offset any potential losses in AET.

Covered calls, and options selling in general, are versatile strategies that can reduce risk, allow you to benefit from short-term market moves and generate income all at the same time.

RSS Feed

RSS Feed